Duolingo cut the humans and crossed $1 billion

50 million daily users, compressed margins, and the AI-first playbook every operator needs to study

Hey Adopter,

Duolingo went all-in on AI in early 2024. The CEO sent a company-wide memo declaring an “AI-first” mandate and told every team that AI proficiency would factor into hiring and performance reviews.

Twelve months later: 50 million daily active users. Over $1 billion in bookings. Nearly 100% of new content generated by machines.

Then the margins shrank, the internet exploded, and the CEO walked back his own memo on camera…

The result that rewrites the operator playbook

Duolingo scaled an AI-first operation to billion-dollar revenue in under two years. But the same playbook cut 10% of the contract workforce, compressed gross margins, and sparked social media meltdowns that reached mainstream news. The gap between the revenue and the fallout is where the real lessons live.

Download the full case study for the strategy, timelines, and measured impact

Daily active users surged 280% between 2021 and 2024, crossing 50 million by end of 2025

Gross margins fell from 73.0% to 71.1%, attributed to generative AI compute costs in SEC filings

Morgan Stanley slashed its price target from $245 to $100

Birdbrain processes roughly 1 billion exercises per day

Content generation automated to nearly 100% across all subjects

Where the money moved

Premium AI features sit behind a $30/month tier. Every video call, roleplay, and tutoring interaction fires expensive LLM API calls. Revenue went up. Margins went down. That tension defines this case.

The contractor trade-off

Duolingo replaced translators and cultural experts with GPT-4 pipelines. Volume scaled overnight. Quality complaints followed just as fast, with users reporting hallucinations, odd phrasing, and missing regional context.

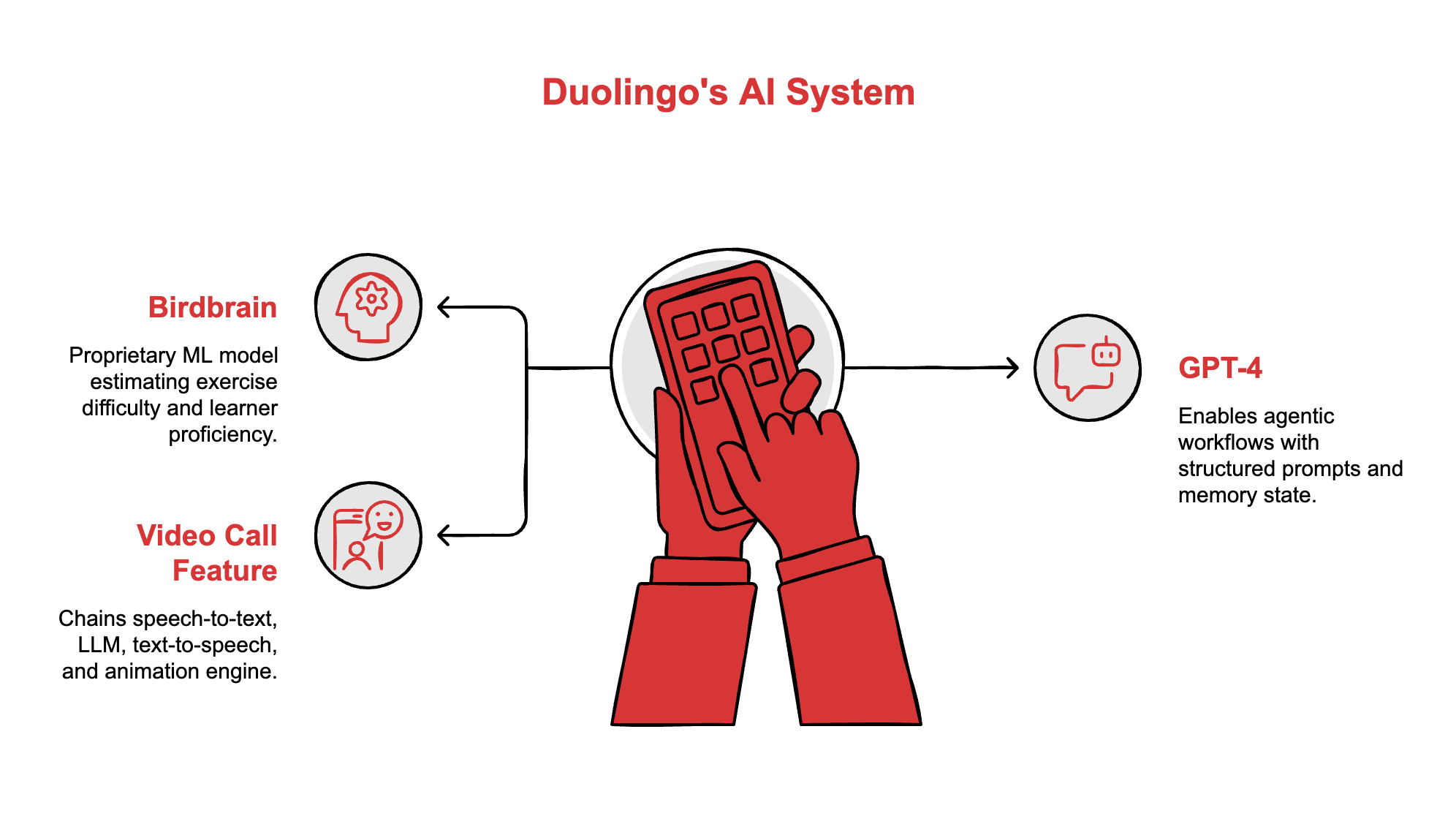

The tech stack behind 50 million daily sessions

Duolingo runs a two-layer AI system. The first layer is Birdbrain, a proprietary machine learning model that has been refined over several years to mimic an expert human tutor. After every single interaction on the platform, Birdbrain simultaneously estimates two things: how difficult a specific exercise is across the entire user base, and where the individual learner sits in terms of proficiency right now. It feeds that data into a session generator that builds custom lessons in real time, keeping the learner in what the team calls the “optimal challenge zone,” not bored, not frustrated.

The second layer is GPT-4. Earlier experiments with GPT-3 failed because the model could not handle unscripted conversation without falling apart. GPT-4 enabled agentic workflows where each interaction runs inside a structured system prompt that defines the AI’s personality, safety guardrails, and allowed tools. Before a conversation starts, the system injects a memory state, things the user mentioned in previous sessions, so the AI feels like it remembers you.

For the Video Call with Lily feature, the architecture chains together speech-to-text, the LLM, text-to-speech, and a real-time 2D animation engine built on Rive. The AI character reacts with facial expressions, lip-syncing, and emotional cues in near-real time. It is the most computationally expensive feature on the platform, and it is also the one driving premium subscriptions.

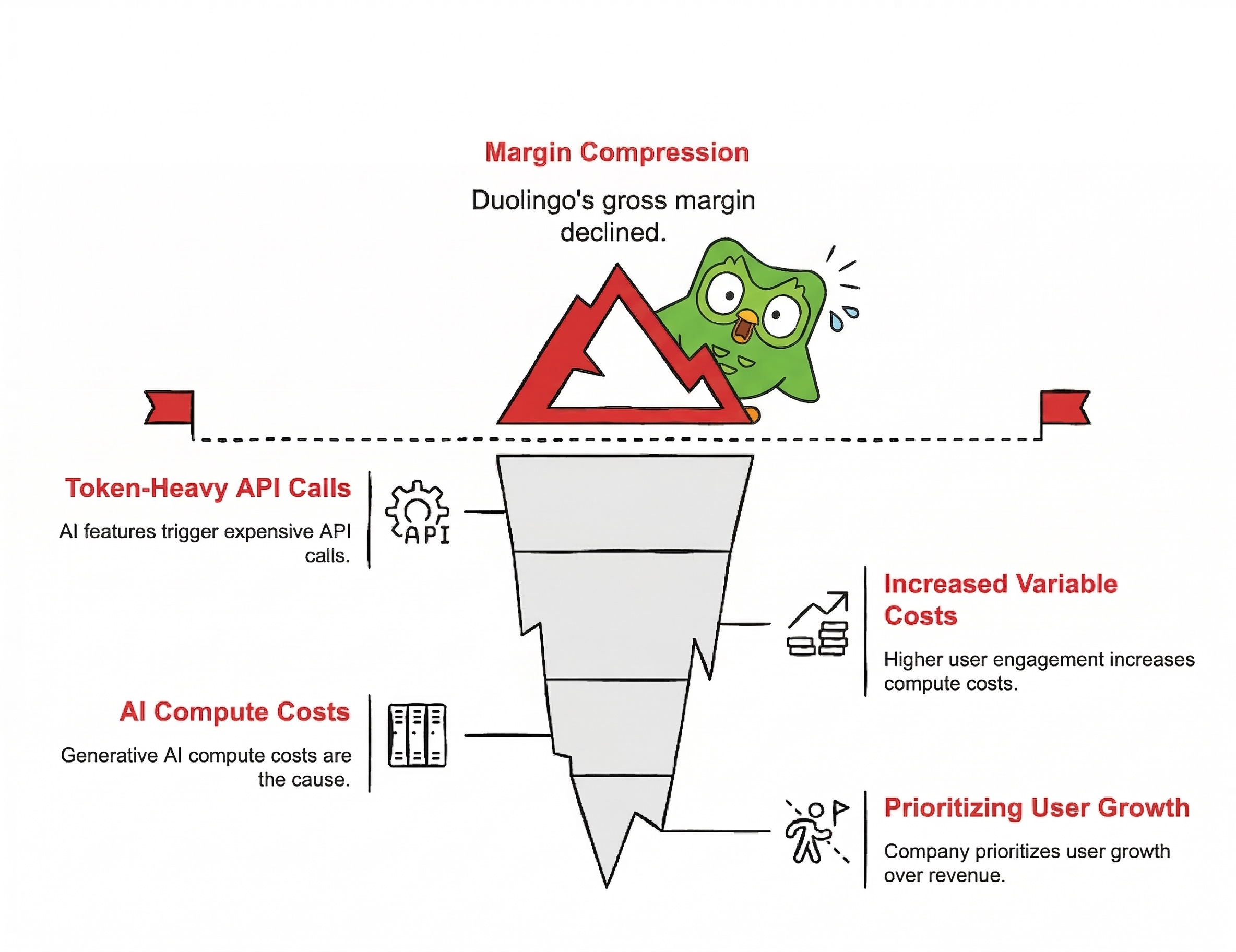

Why margins compress when AI features succeed

Traditional SaaS economics reward scale. Build the software once, and every new user costs almost nothing. AI features break that model. Each Duolingo Max session triggers token-heavy API calls to large language models. The more users engage with the best features, the higher the variable costs climb.

Duolingo’s gross margin dropped from 73.0% in early 2024 to 71.1% in early 2025. The company attributed the decline directly to generative AI compute costs tied to the Max tier expansion. Their shareholder letter confirmed $305.9 million in adjusted EBITDA on a 29.5% margin, strong by most standards, but the downward trajectory on gross margin caught Wall Street’s attention.

Morgan Stanley responded by cutting the price target from $245 to $100 and flagging concerns about the company prioritising user growth over near-term revenue. The board authorised a $400 million share repurchase programme to stabilise the stock.

For any operator watching this: if your AI features succeed, your compute bill grows with them. Budget for it before you launch, not after.

The human cost and the trust gap

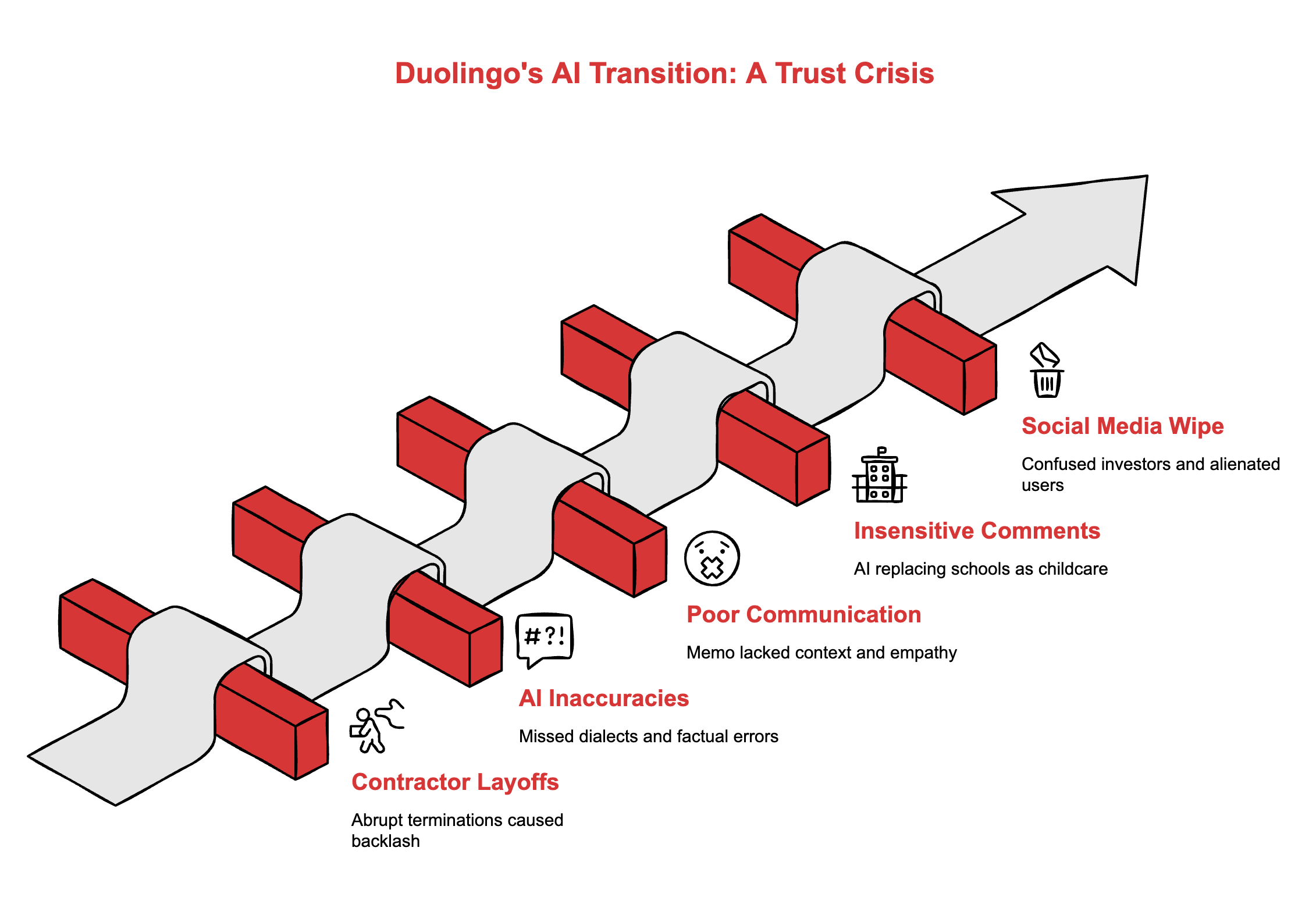

Duolingo cut roughly 10% of its contract workforce in early 2024, replacing translators, curriculum designers, and cultural experts with automated pipelines. The CEO’s internal memo stated the company would “gradually stop using contractors to do work that AI can handle.”

The public reaction was brutal. Former contractors spoke publicly about abrupt terminations. Linguists pointed out that AI-generated courses missed regional dialect differences that carry serious social weight, like the distinction between formal and informal address in Latin American Spanish. Users flagged hallucinations where the AI provided incorrect historical dates, repeated words nonsensically, or defended wrong grammar rules when questioned.

The CEO later admitted on stage at the Fast Company Innovation Festival that the communication was his fault. He said the memo “really struck a nerve” and that he “did not give enough context.”

Separate from the contractor controversy, the CEO’s public comments on a podcast, where he suggested AI would handle most education and schools would function as “childcare,” drew condemnation from educators and union advocates globally.

The combined damage forced Duolingo to wipe its social media accounts in May 2025 in a crisis stunt that confused investors and alienated users even further.

The 30-60-90 plan if you are running a similar pivot

Days 1 to 30: audit and baseline

Map every content workflow that currently depends on human labour. Measure cost per unit, turnaround time, and quality score. Identify which tasks are repetitive and high-volume versus which require cultural judgment or creative nuance. Set baseline metrics before changing anything.

Days 31 to 60: pilot with guardrails

Select one high-volume, low-stakes content workflow and automate it with an LLM. Keep a human reviewer in the loop for every output. Track cost savings alongside quality metrics. If the AI output requires more than 20% human editing, the workflow is not ready for full automation.

Days 61 to 90: scale or stop

If pilot results hold, expand to the next workflow. If quality degrades at volume, add reviewer capacity before scaling further. Build a margin model that includes compute costs per interaction, not just per user, so you know your break-even point before you hit it.

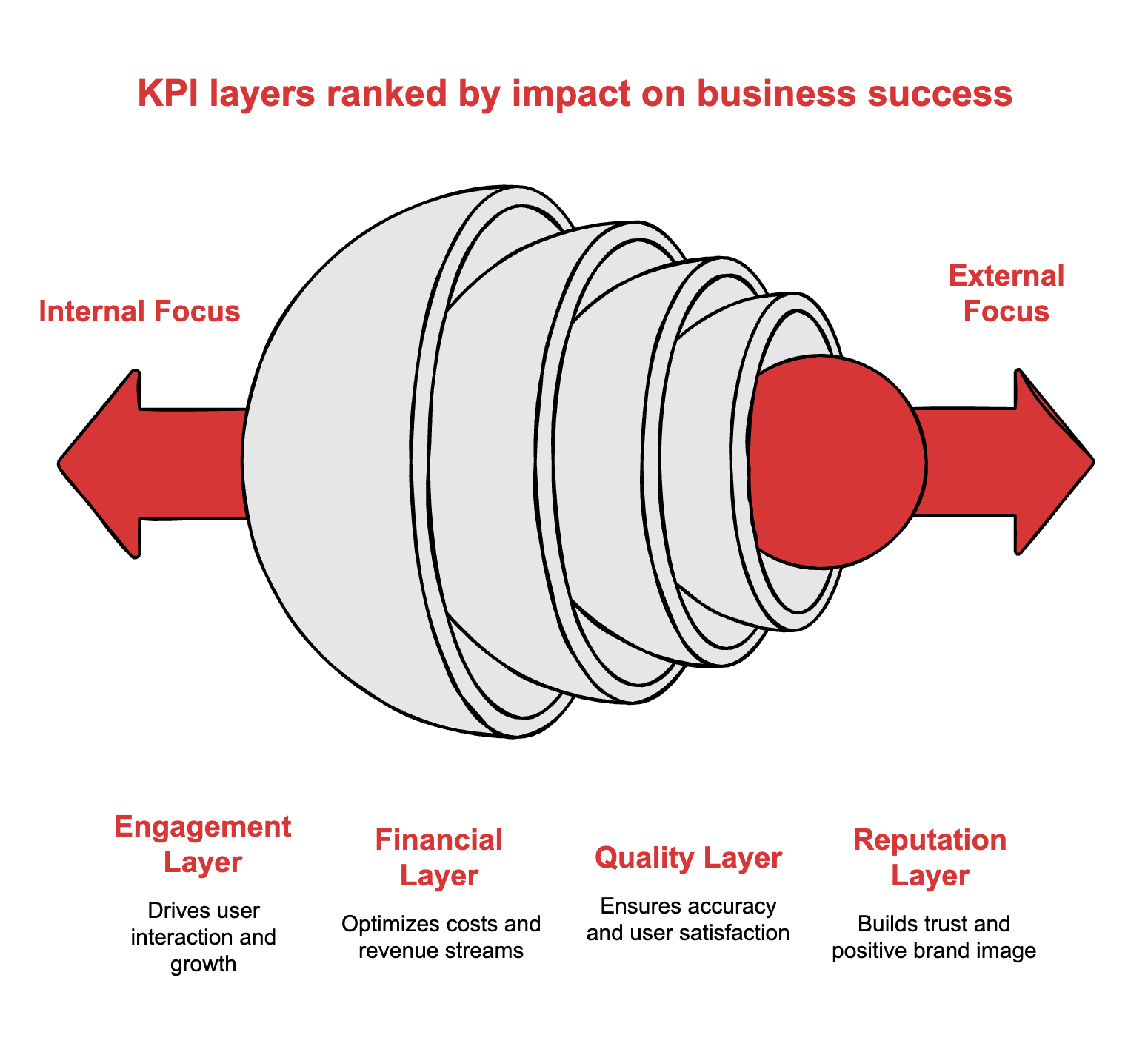

KPI tree and targets

Engagement layer: daily active users, session length, feature adoption rate for AI tools. Duolingo tracked DAU growth obsessively, hitting 280% growth over three years.

Financial layer: gross margin by product tier, compute cost per AI interaction, average revenue per user. The 190-basis-point margin compression is the number to watch. If your AI tier grows faster than your ability to optimise inference costs, the margin gap widens.

Quality layer: content accuracy rate, human review rejection percentage, user-reported error volume. Duolingo’s failure here is the cautionary piece. Track hallucination rates and user complaints per thousand interactions from day one.

Reputation layer: net promoter score, social sentiment, contractor and employee satisfaction. This is where Duolingo lost control. Measure it or accept that you will be blindsided.

What to do next

Audit your highest-volume content workflows this week and tag each one as “automate now,” “automate with review,” or “keep human”

Build a per-interaction cost model before you commit to any AI-powered feature at scale

Keep at least one human reviewer in every automated pipeline until your quality metrics prove you do not need them

Adapt & Create,

Kamil

References and source notes

Duolingo reports fourth quarter and full year 2025 results , Duolingo Investor Relations, 2026. Primary source for DAU milestones, $1B+ bookings, $305.9M EBITDA, and $400M buyback authorisation.

Shareholder letter, Duolingo Investor Relations , Duolingo, 2025. Detailed EBITDA margins, free cash flow of $360.4M, and expansion into maths, music, and chess.

Case study on Duolingo’s AI-powered language learning revolution , 5D Vision, 2025. CEO quote on automating content generation to nearly 100%.

Q1 FY25 shareholder letter , Duolingo, 2025. SEC filing attributing gross margin decline from 73.0% to 71.1% to generative AI compute costs.

Duolingo’s AI-first strategy explained , AI Magazine, May 2025. Details on the 2024 internal memo and CEO’s comparison to the 2012 mobile-first pivot.

AI-first, Duolingo plans to cut contractor roles , HRD America, 2024. Reporting on the mandate to stop using contractors for AI-replaceable work.

Duolingo CEO, no layoffs since AI-first announcement , HRD America, September 2025. CEO admitting communication failure at Fast Company Innovation Festival.

Duolingo lays off 10% of contractors amid AI push , OECD.AI, 2024. Independent documentation of contractor displacement scale.

Morgan Stanley reiterates equal weight rating for Duolingo , MarketBeat, February 2026. Price target reduction from $245 to $100.

How Duolingo’s AI-first strategy lost the human touch , Solutions Review, 2025. User and linguist complaints about cultural nuance loss and content quality degradation.

My AI is lying to me, user-reported LLM hallucinations in AI mobile apps reviews , PMC, 2026. Peer-reviewed study categorising hallucination types reported by Duolingo users.

Birdbrain introduction , Duolingo Blog. Technical overview of the dual-estimation personalisation engine processing ~1 billion exercises daily.

Building Duolingo-style AI video call characters using Rive , DEV Community, 2025. Technical breakdown of the speech-to-text, LLM, TTS, and animation rendering pipeline.

This is a really solid breakdown, but I think the framing slightly overstates the margin compression as an AI-specific problem.

Duolingo went from 73% to 71.1% gross margin — that's a 190 basis point drop while simultaneously scaling DAU by 280% and crossing $1 billion in bookings.

Most operators would take that trade happily. Isn't the real cautionary tale here less about AI economics and more about the PR mismanagement?

The unit economics seem workable; what actually cratered the stock was a CEO who couldn't read the room.... If Duolingo had quietly automated and kept contractors on in smaller roles as quality reviewers, would anyone be writing this as a warning story instead of a success story?