Payment Giants Spent $14 Billion on AI, Here's What Worked

A step-by-step guide based on real failures from Mastercard and others

Hey Adopter,

TLDR: Visa, Mastercard, AmEx, and Discover invested $14 billion in AI over the past decade. Fraud detection delivered massive returns, customer service automation flopped hard, and one company's failed integration cost $190 million plus 1,000 jobs. The lessons translate directly to SMB AI strategy.

If you are not ready to become a Premium Subscriber, you can purchase this case study by itself, including a study guide, an audio overview, and a video overview of the findings.

Mastercard lost $190 million and laid off 1,000 people because their AI integration failed spectacularly.

The four payment networks, Visa, Mastercard, American Express, and Discover, have moved beyond AI experimentation into production-scale deployment. Their combined infrastructure investments exceed $14 billion over the past decade. Yet beneath the marketing rhetoric lies a stark reality: whilst fraud detection applications delivered measurable returns, ambitious projects in customer service automation stumbled badly.

The stakes are clear. Visa processes 300 billion transactions annually through AI systems that prevented $40 billion in fraud last year. Mastercard claims up to 300% improvement in fraud detection rates. American Express maintains the industry's lowest fraud rates for 14 consecutive years through AI. But when these giants tried full customer service automation, customers revolted and satisfaction plummeted.

What worked: the defensive plays

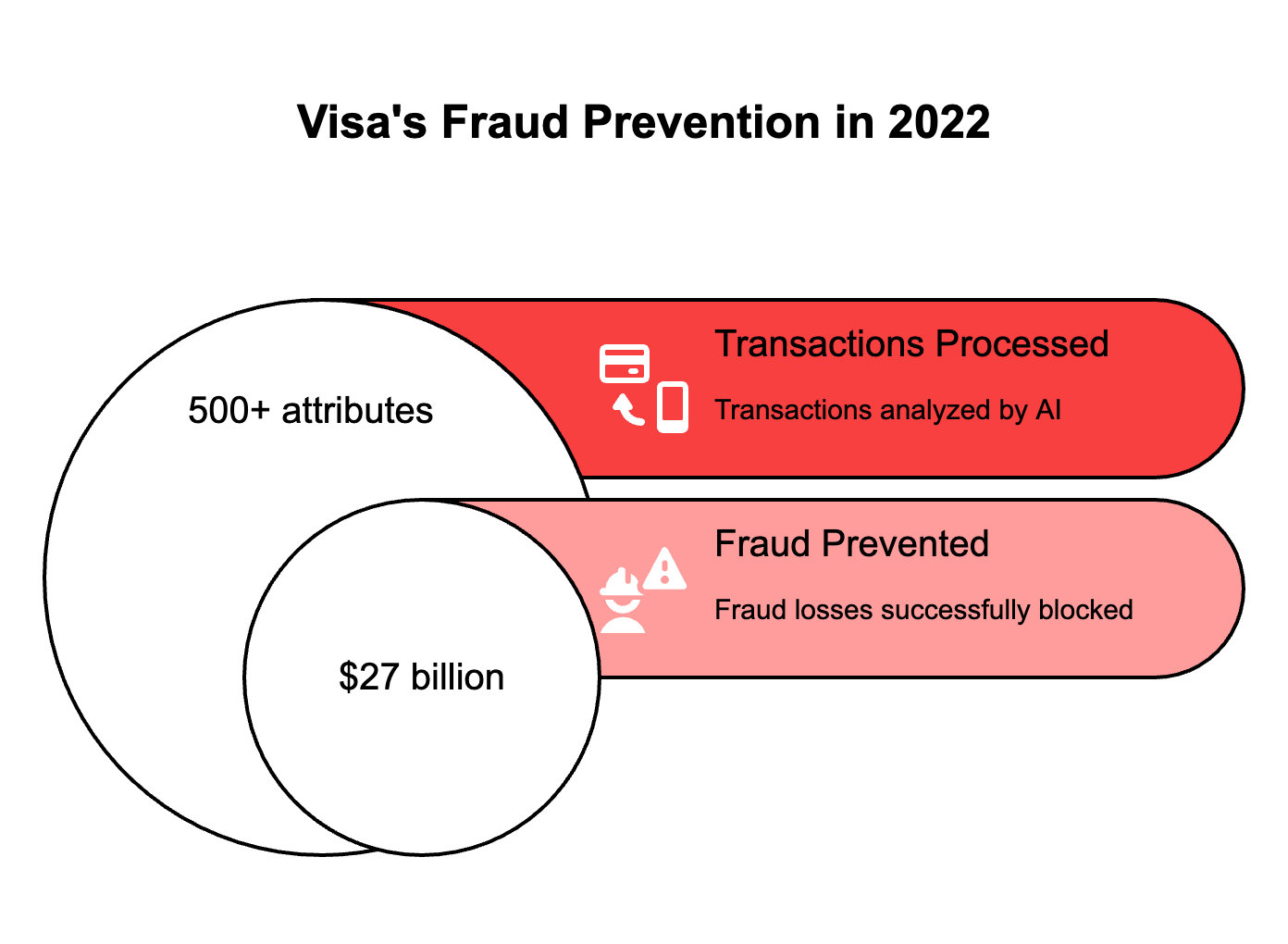

Real-time fraud detection represents the payment industry's biggest AI success story. Visa's Advanced Authorization system processes every transaction across their network in under 50 milliseconds, analysing 500+ attributes through hundreds of AI models. The system prevented $27 billion in fraud in 2022 alone.

The secret lies in the economic model. Each transaction costs roughly $0.0001 in AI processing whilst preventing fraud losses averaging $50-500 per blocked fraudulent transaction. This creates a cost-benefit ratio exceeding 500:1 for successfully prevented fraud.

For SMBs, this suggests focusing AI investments on high-stakes, measurable problems where the cost of failure far exceeds the cost of prevention. Think inventory shrinkage detection, quality control automation, or customer churn prediction rather than flashy chatbots.

American Express demonstrates another winning approach: behavioural biometrics. Their system monitors typing patterns, device usage, and interaction behaviours to detect account takeovers before fraudulent transactions occur. The result: 50% reduction in false positives whilst maintaining 95% detection accuracy.

The SMB translation: start with simple pattern recognition in your business. Customer behaviour analysis, supplier payment patterns, or employee productivity metrics often reveal actionable insights without complex infrastructure.

What failed: the automation trap

Customer service automation represents the industry's biggest disappointment. Despite massive investments, J.D. Power data shows declining customer satisfaction with automated credit card support. Customers rate automated tools poorly for handling "anything other than very basic activities."

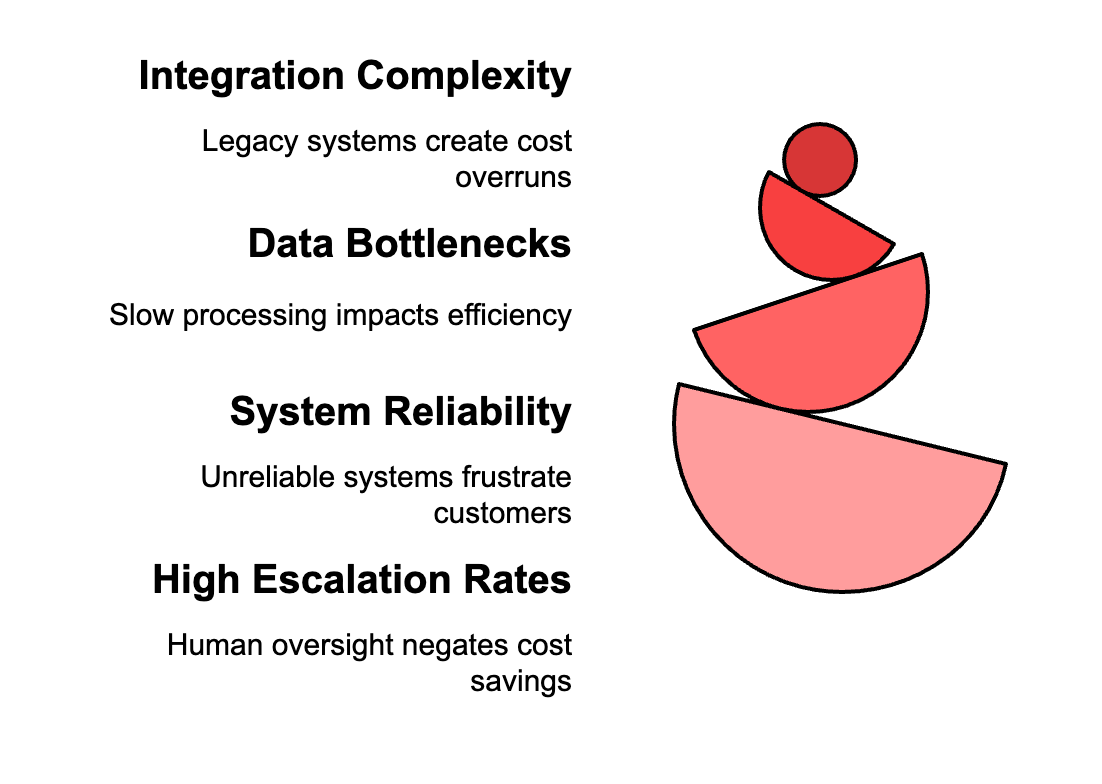

Discover's Google Cloud AI integration achieved 70% improvement in call handle time, yet still requires significant human oversight for complex issues. The promised cost savings evaporated when escalation rates remained high.

Mastercard's experience provides the starkest warning. The company's AI integration challenges led directly to 1,000 layoffs and a $190 million restructuring charge. Integration complexity with legacy systems, data processing bottlenecks, and system reliability issues created costs far exceeding initial projections.

The lesson for smaller businesses: avoid the temptation to automate customer-facing interactions completely. Focus AI on behind-the-scenes efficiency rather than replacing human judgement entirely.

But there's a deeper story here about implementation strategy, vendor selection, and the hidden costs that can make or break AI projects. The payment giants' experiences reveal three critical frameworks that determine success or failure, plus a counterintuitive approach to AI adoption that most businesses get backwards.

The biggest lesson? It's not about the technology you choose, it's about the sequence you choose it in. Get this wrong, and you'll join Mastercard in expensive restructuring. Get it right, and you'll build sustainable competitive advantages.

Here's what the full case study reveals:

The exact vendor selection criteria that prevented American Express from Mastercard's fate

Why Discover's "boring" vendor-led approach delivered better ROI than Visa's $100 million innovation fund

The three-stage AI adoption framework that successful payment companies follow

How to calculate the true cost of AI implementation, including hidden integration expenses

The emerging competitive threats that will reshape the industry in 2026